Callicles to Socrates: “What you say is of no interest to me, and I will continue to act as I have previously, without worrying about the lessons you claim to give.” Gorgias, Chapter 3

Only 8% of the jobs in the United States are now in industry. Donald Trump, the new President of the United States, wants to reindustrialize America and is speaking out against the opening of factories abroad and the closing of local factories. Is there any economic rationale for the indiscriminate communications of the new US President?

Trump’s statements about manufacturing abroad by major American corporations are disturbing to an economist. It is as if threatening the multinationals, raising tariffs on their imports, and menacing them with punitive taxes will suffice to get them to reconsider their decisions to outsource. Beyond the fact that Trump’s method is the antithesis of the rule of law, what is surprising to an economist is that these statements ignore not only everything that is known about the logic of globalizing value chains but also the nature of past trends in industrial production and its future prospects. They therefore raise more perplexity than support (see the note of X. Ragot on macroeconomic policy).

The only truth in Trump’s rhetoric is the fact of intense American deindustrialization. So let’s start from the state of American industry to understand the grounds for the working-class nostalgia on which this rhetoric is based.

America’s worn-out industrial fabric – fertile terrain for blue-collar nostalgia

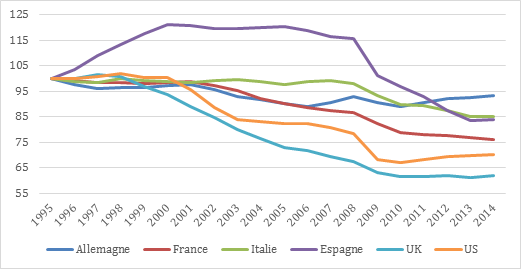

Donald Trump taps into the wellsprings of voter nostalgia for a time when the manufacturing sector was in full swing. It is clear that America’s deindustrialization was intense, even though it opened up commercially much less than Europe did. For the many workers who lack social protection it has been brutal. The countries where the discourse in favor of re-industrialization has been most widespread are those where the decline in industrial employment was most pronounced, namely the United States, the United Kingdom and France. All three have lost more than a quarter of manufacturing jobs since 1995[1].

Figure 1: Changes in jobs in manufacturing (base 100 in 1995)

Source: EU Klems for European countries. Federal Bank of St Louis (FRED) for the United States.

Figure 1 shows the similarity in the trends in these three economies since the end of the 1990s: France started to lose jobs a little after the United States and United Kingdom, and the end of this trend, which can be seen in the US and UK as of 2009, is still not clearly visible in France, which has continued to shed jobs, although at a slower pace than at the beginning of the period.

The United States lost more than 5 million jobs since 1995, compared to more than 1.5 million in the United Kingdom and 900,000 in France, representing 29%, 38% and 24%, respectively, of the losses over the period. Of course, at first gains in productivity permitted a smaller decline in value-added, but this was less the case from 2000 onwards, given the slowdown in productivity gains in the manufacturing sector. It should also be noted that manufacturing employment has risen since 2010 in the US, but once again slowed from 2015 (see Bidet-Mayer and Frocain, 2017).

The causes of deindustrialization have been clearly identified. Deindustrialization has affected all the old industrial powers because of both technical progress and the shift of manufacturing value into industrial services. At the global level, manufacturing output now represents only 16% of GDP, making the 12% American level quite honorable. Moreover, the United States is still a major player in global manufacturing, second only to China in the volume of production.

Finally, once it is understood that the incorporation of technology in manufacturing value-added will not slow its pace and that the robotization of the repetitive tasks specific to mass production will continue or even accelerate, it is certain that future industrial production will be even less job-rich (on this topic see M. Muro).

In terms of the rise of the Trump electorate, only a small fraction of the voters located in a small part of the northern United States were actually victims of deindustrialization. But industry is a symbolic sector, an emblem of the economic power of yesteryear, of martial imperial power, of the birth of the consumer society and then of the emergence of Asia’s economic powers, the new homes of the world’s factories. This particularly affects a section of the middle and working class that has not seen its income improve over the last 20 years (as is suggested in the “elephant” graphic of Branko Milanovic)[2]). Finally, America’s deindustrialization can be seen as symmetric with the industrialization of China and other emerging countries like Mexico, whose economic success is taken as a scapegoat by this middle class. But while globalization has had differentiated effects on individuals based on their qualifications, it cannot be superimposed on deindustrialization.

Starting from this nostalgia for the industrial might of yesteryear, Trump chose to become personally involved in companies’ outsourcing decisions in order to win the vote of these middle class forces who’d suffered from deindustrialization. His interventions have consisted in directly going after companies by calling on them to modify their decisions. Let’s take a look at the most striking episodes in order to grasp the respective motivations of the actors.

Symbolic, eye-catching industrial symbols

First there was the case of Carrier, an equipment manufacturer in Indiana that makes heaters and air conditioners, which in February 2016 announced its decision to move 1,400 jobs to Mexico. Having seized on this case during his campaign, once elected Trump went on to negotiate in November with the heads of the company. In exchange for relief on taxes, charges and regulations, Trump demanded that some of the jobs be kept in Indiana. The local authorities also joined in the negotiations in an effort to coax the company. On November 30, the company announced its intention to retain 1000 jobs on the site. This victory was highly symbolic, in every sense of the word, given that the American economy creates more than 180,000 jobs every month. Carrier’s parent company, United Technologies, conceded that this turnaround will not cost it that much, especially if it gets an attentive ear from the President, and also because United Technologies is a manufacturer of military equipment and is heavily dependent on public procurement (10% of its sales according to the New York Times).

Then there was the episode involving Foxconn, a Taiwanese company that assembles products by Apple – its biggest customer – that decided to set up an assembly plant in the United States, a decision that Trump then brandished as a personal victory. Foxconn already owns production units in the US. This was not a priori a relocation of activities, as the company does not envisage simultaneously “disinvesting” in Taiwan. If the company decides to invest in the US, it is because it has good reasons to do so. Among these are expectations about the growth of the US market, the trade obstacles that Trump is threatening to erect and the pressure that its main client (Apple) might bring to bear.

Finally, Trump has tackled the automotive industry. He had already lambasted Ford Motors’ plan to build a plant in Mexico back in the spring of 2016. On 3 January 2017, the company decided to cancel its USD 1.6 billion project in the state of San Luis Potosi in Mexico and announced a USD 700 million investment in a plant in Flat Rock, Michigan, to build electric cars and autonomous cars. Was this a turnaround by the company? In fact, the Mexican plant was designed to build the Ford Focus, small models for which demand has fallen sharply in favour of SUVs and other “crossovers”. Ford’s decision indicates that it is trying to reduce production of this range of vehicles, while Trump’s policy should lead to a revival of American demand for automobiles outside this range. The car maker is nevertheless confirming its decision to shift its production capacity for the Focus model from Wayne, Michigan to Hermosillo, Mexico (The Economist, Wheel Spin, 2017). These decisions therefore reflect more a repositioning by the company rather than a relocation.

The threat of a 35% customs duty on vehicles from Mexico or a tax on revenue from imports is obviously being taken seriously by manufacturers. In 2015, the United States imported more than 2 million vehicles from Mexico. Car makers have every interest in showing clean hands in order to obtain other benefits, such as the relaxation of emission regulations. In addition, with the ex-president of ExxonMobil, Rex Tillerson, assuming the post of Secretary of State and defending fossil fuels and Trump’s economic recovery programme, manufacturers anticipate a pick-up in purchases.

The series of challenges and reactions is continuing (Hyundai, Toyota, BMW, etc.). Trump is going through all the manufacturers and suspects that any production overseas represents a raid on American jobs. It is not by chance that he is focusing on the automotive industry, as this sector is emblematic of the American way of life, a symbol of US industrial power at a time when the rust belt was still glitzy. But the sector is now highly globalized, and one wonders how at this point Trump can ignore or deny the way the industry is organized and go on deceiving his supporters.

Is there really a pool of jobs to relocate?

Globalization can affect the way companies organize production in two ways. First, in combination with technical progress, it can lead to the disappearance of manufacturing following complete outsourcing, while maintaining control over the chains where profits are realized. This is for instance the case of Apple, which does not have its own plants abroad. Apple cannot be compelled to bring back what it has not taken away! If tariffs increase, Apple will import more expensive components, the State will recover part of the rent from innovation and consumers will pay part of the tax. Second, globalization may also result in outsourcing production, and in this case the company does own production sites abroad, such as in the automotive sector as well as in textiles and toys, like Mattel. Jobs have indeed been displaced, but sometimes the skills as well, which it is not necessarily easy to find again in the home country.

Mexico’s cost advantage is also not about to disappear: the wage costs in Indiana per hour are equivalent to the wage costs in Mexico per day. The same is true for the cost in China. The relocation of this type of employment would entail a sharp drop in wages, unless higher customs duties (which raise foreign wages), lower energy and tax costs and higher productivity (which reduce American wages) led to a new trade-off. But this would require major changes that would inevitably impact the rest of the non-manufacturing economy, i.e. 92% of jobs.

In the end, the job content of imports is not “relocatable” in its entirety. Moreover, a large portion of imports fuel exports: in other words, a major part of Chinese and Mexican jobs activate American jobs whose output is sold abroad because the development of the emerging countries has led to the solvency of demand. There is such interdependence today that no one knows what the consequences of a new employment equilibrium would be for future prices, profits, investments and jobs.

What would be the consequences of industrial relocation?

Consider again the case of Foxconn. If this company invests, it would be to serve the US market. Since production costs are higher there, this implies three possible non-mutually exclusive strategies. The company cuts its margins (Apple too) in order not to reduce its market share: Foxconn and Apple accept this reduction in margins in order to offset the negative impact on sales due to the stigma cast by Trump on the company. The second strategy would be to increase the prices of products on the US market: this would mean consumers are financing the few jobs created. The third strategy: the company develops different production processes, including intensive automation that cuts the labour costs while also reducing logistics costs to serve the US market. At the end of the day, Foxconn’s decision, if it is confirmed, is a fairly standard economic rationale. The Trump effect figures in this mix in so far as it requires Apple to justify its strategy of localization. But if Trump’s messages were to jeopardize the company’s financial health (though it does of course have margins), then this would jeopardize a flagship of the US economy.

In the case of manufacturers, the multiplication of investments, if confirmed, will inflate both the supply of labour as well as supply of domestic production. This would increase competition among businesses. Not only would wages increase, but margins would be reduced due to higher production costs, higher prices for imported components and heightened competition in the domestic market. It is far from certain that it is US manufacturers who would come out on top. At that point, if it came to accepting the Chinese taking holdings in their capital, they would be hoisted on their own petard! The investment decisions taken by the car makers as a whole could even result in labour shortages – the US job market is close to full employment – leading to higher wages (and hence production costs), resulting in turn in either accelerating robotization or bringing in foreign workers.

So ultimately, if we ask ourselves what would be the impact of additional investments on America, it all depends on what incentives they are responding to. If these respond to new, tighter constraints being put on companies by the new government, then microeconomic theory tells us that a company’s output will fall or else be more expensive. If an external event increases a company’s costs, it produces less 1) either immediately because it increases its prices, or 2) in the medium to long term because its margins are falling (it has not increased its prices) and it is investing less, or 3) in the long term because it leaves the market. If they are responding to expectations of an increase in demand, then Trump will need to stick to his promises of a recovery. Finally, if investment is made in exchange for fiscal expenditure (lower taxes, investment subsidies, financial support), then the cost to the public purse will result in lower present or future expenditure. In short, the investment will take place if it benefits the company: whether it locates in the country of origin or abroad, it is always conditional on the promise of future income.

But why defend the multinationals and renounce protectionism?

Proponents of protectionist measures respond: 1) what does it matter if firms produce less in total, if the distribution of their output is more advantageous to the domestic territory; 2) what does it matter if they make less profit, as these multinationals already make so much! This neglects that companies also have integrated strategies – that is, global strategies – and that if they earn less profits, they will invest less, which will eventually impact their future growth. It also neglects that the multinationals are the ones that invest the most in R&D, and that if their stock market value rises they do not distribute all the dividends. It neglects that trade, while not balanced, is bilateral, that is, if we reduce the incomes of our partners by reducing their exports, we reduce our own exports. In other words, if the income of Mexicans falls substantially, they will buy a lot less American goods. Furthermore, protectionism – which always winds up being bilateral (retaliation requires it) – protects not the weak, but the profiteers.

Some argue that protectionist measures are a means of relocating production sites to consumption sites (in order to avoid barriers), and hence to recover activities that have been outsourced. It must be emphasized that protectionism protects the giants, the businesses that can deal with tariff barriers. And while it saves unskilled jobs a little longer, it maintains them in their “unskilled” state. Above all, it hampers the development of a middle class of both consumers and businesses. Inequalities will not be reduced through protectionism; instead, the society and the economy will freeze up. Protectionism is not the solution to the differentiated gains coming from globalization.

In the United States, the effects of globalization have been relatively pronounced, and despite a dynamic labour market, the distribution of the gains from growth has been very uneven. The constraints on skills adjustments have been intense: thus, the 12% of manufacturing value-added, while very honorable, is concentrated mainly in the electronics and information technologies sector (see Baily and Bosworth, 2016). A recent work by D. Autor and his co-authors at MIT demonstrates that the exposure to Chinese imports has led to polarizing votes towards candidates at the extremes of the political spectrum. This reveals the strong sensitivity of voters to the hallmarks of globalization.

Yet while the malaise is real, protectionist measures cannot fundamentally heal it because they will diminish the economic wealth of less well-off groups whose consumption basket contains relatively more imported products, whereas few jobs will be created. Let’s look once again at the case of the automobile sector, where the American consumer will see car prices go up: the purchasing power of consumers as a whole will go to the benefit of a small minority of workers in the automobile sector. The reduction in corporate taxation will reduce fiscal revenues and the resources for financing the public goods that benefit less well-off strata the most. And it is not at all certain that this reduction in taxation will have a positive impact on business if at the same time the latter also incurs additional customs duties.

In conclusion, industrial employment will not be revived by protectionist measures. Nor will it lessen the economic malaise of the middle class. With an economic and foreign policy that accentuates the present imbalances – isolationism, protectionism, the revival of full employment – Donald Trump is voluntarily taking his mandate into unstable, unknown territory. The cynical pragmatism of the world’s economic players will not be stamped out by Trump’s rhetoric, which will instead undoubtedly generate another type of cynicism, one marked by the horizons of an unexpected, personal mandate, with every man for himself.

[1] Manufacturing is a major subset of industry that excludes the energy business. It is common to associate industry with the manufacturing sector.

[2] Branko Milanovic, Global Inequality, 2016, HUP.

Leave a Reply