By Anne-Laure Delatte and Henri Sterdyniak

The plan that has just been adopted sounds the death knell for the banking haven in Cyprus and implements a new principle for crisis resolution in the euro zone: banks must be saved by the shareholders and creditors without using public money. [1] This principle is fair. Nevertheless, the recession in Cyprus will be deep, and the new extension of the Troika’s powers further discredits the European project. Once again the latest developments in the crisis are laying bare the deficiencies in euro zone governance. It is necessary to save the euro zone almost every quarter, but every rescue renders the zone’s structure even more fragile.

Cyprus never should have been accepted into the euro zone. But Europe privileged expansion over coherence and depth. Cyprus is a banking, tax and regulatory haven, which taxes companies at the rate of only 10%, while the balance sheet of its oversized banking system is nearly eight times its GDP (18 billion euros). Cyprus is in fact a transit hub for Russian capital: the Cypriot banks have about 20 billion euros in deposits from Russia, along with 12 billion euros in deposits of Russian banks. These funds, sometimes of dubious origin, are often reinvested in Russia: Cyprus is the largest foreign investor in Russia, to the tune of about 13 billion euros per year. Thus, by passing through Cyprus, some Russian capital is laundered and legally secured. As Europe is very committed to the principle of the free movement of capital and the freedom of establishment, it has simply let this go.

Having invested in Greek government debt and granted loans to Greek companies that are unable to pay due to the crisis, the island’s oversized banking system has lost a lot of money and has fostered a housing bubble that burst, resulting in heavy losses. Given the size of the banking system’s balance sheet, these losses represent a significant share of national GDP. The banking system is in trouble, and as a consequence the markets speculated against Cypriot government debt, interest rates rose, the country plunged into a recession, and the deficit deepened. In 2012, growth was negative (-2.5%); the deficit has reached 5.5% of GDP, the public debt has risen to 87% of GDP, the trade deficit stands at 6% of GDP, and the unemployment rate is 14.7%.

The country needed assistance both to finance itself and to recapitalize its banks. Cyprus requested 17 billion euros, the equivalent of its annual GDP. Ten billion euros of loans were granted, of which nine will be provided by the ESM and one by the IMF. From a financial point of view, the EU certainly did not need that billion, which merely gives the IMF a place at the negotiating table.

In exchange, Cyprus will have to comply with the requirements of the Troika, i.e. reductions of 15% in civil servant salaries and 10% in spending on social welfare (pensions, family allowances and unemployment), the introduction of structural reforms, and privatization. It is the fourth country in Europe to be managed by the Troika, which can once again impose its dogmatic recipes.

Cyprus is to lift its tax rate on corporations from 10 to 12.5%, which is low, but Europe could not ask Cyprus to do more than Ireland. Cyprus must increase the tax rate on bank interest from 15 to 30%. This is a timid step in the direction of the necessary tax harmonization.

But what about the banks? The countries of Europe were faced with a difficult choice:

– helping Cyprus to save its banking system amounted to saving Russian capital with European taxpayers’ money, and showed that Europe would cover all the abuses of its Member States, which would have poured more fuel on the fire in Germany, Finland and the Netherlands.

– asking Cyprus to recapitalize its banks itself would push its public debt up to more than 150% of GDP, an unsustainable level.

The first plan, released on 16 March, called for a 6.75% contribution from deposits of less than 100,000 euros and applied a levy of only 9.9% on the share of deposits exceeding this amount. In the mind of the Cypriot government, this arrangement had the advantage of not so heavily compromising the future of Cyprus as a base of Russian capital. But it called into question the commitment by the EU (the guarantee of deposits under 100,000 euros), which undermined all the banks in the euro zone.

Europe finally reached the right decision: not to make the people alone pay, to respect the guarantee of 100,000 euros, but to make the banks’ shareholders pay, along with their creditors and holders of deposits of over 100,000 euros. It is legitimate to include those with large deposits that had been remunerated at high interest rates. It is the model of Iceland, and not Ireland, that has been adopted: in case of banking difficulties, large deposits remunerated at high rates should not be treated as public debt, at the expense of the taxpayers.

Under the second plan, the country’s two largest banks, the Bank of Cyprus (BOC) and Laiki, which together account for 80% of the country’s bank assets, are being restructured. Laiki, which was hit hardest by developments in Greece and which was more heavily involved in the collection of Russian deposits, has been closed, with deposits of less than 100,000 euros transferred to the BOC, which takes over Laiki’s assets, while it also takes charge of the 9 billion euros that the ECB has lent it. Laiki customers lose the portion of their deposits over 100,000 euros (4.2 billion), while holders of Laiki equities and bonds lose everything. At the BOC, the excesses of deposits above 100,000 euros are placed in a bad bank and frozen until the restructuring of the BOC is completed, and a portion of these (up to 40%) will be converted into BOC shares in order to recapitalize the bank. Hence the 10 billion euro loan from the EU will not be used to resolve the banking problem. It will instead allow the government to repay its private creditors and avoid a sovereign bankruptcy. Remember that the national and European taxpayers are not called on to repair the excesses of the world of finance.

This is also a first application of the banking union. Deposits are indeed guaranteed up to 100,000 euros. As requested by the German government, the banks must be saved by the shareholders and creditors, without public money. The cost of bailing out the banks should be borne by those who have benefited from the system when it was generating benefits.

From our viewpoint, the great advantage is ending the poorly controlled financial status of Cyprus. It is a healthy precedent that will discourage cross-border investment. It is of course regrettable that Europe is not attacking other countries whose banking and financial systems are also oversized (Malta, Luxembourg, the United Kingdom) and other regulatory and tax havens (the Channel Islands, Ireland, the Netherlands), but it is a first step.

This plan is thus well thought-out. But as was modestly acknowledged by the Vice-President of the European Commission, Olli Rehn, the near future will be very difficult for Cyprus and its people. What are the risks?

Risk of a deposit flight and liquidity crisis: unlike the initial plan, which called for a levy on all deposits, the new plan is consistent with reopening the banks relatively quickly. In fact, the banks are staying closed as long as the authorities fear massive withdrawals by depositors, which would automatically lead to a liquidity crisis for the banks concerned. However, as small depositors are not affected and large depositors have their assets frozen until further notice, it seems that the risk of a bank run can be ruled out. A problem will nevertheless arise when the large deposits are unfrozen. Their almost certain withdrawal will very likely result in a loss of liquidity for the BOC, which will need to be compensated by specially provided liquidity lines at the ECB. Some small depositors who take fright could also withdraw their funds. Similarly, holders of large deposits in other banks, although in less difficulty and thus not affected, could worry that the levies will be extended in the future and therefore try to move their money abroad. Cyprus remains at the mercy of a liquidity crisis. This is why the authorities have announced exceptional controls on capital movements when the banks reopen, so as to prevent a massive flight of deposits abroad. This is a novelty for the EU. But the transition, which means shrinking the Cypriot banking sector from 8 times the island’s GDP to 3.5 times, could well prove difficult and may have some contagion effects on the European markets, since the banks will have to sell a significant amount of assets.

Risk of a long recession: the halving of the size of the banking sector will not take place painlessly, as the entire economy will suffer: bank employees, service partners, attorneys, consultants, auditors, etc. Some Cypriot companies, along with some wealthy households, will lose part of their bank holdings.

However, the plan requires simultaneous fiscal austerity measures (on the order of 4.5% of GDP), structural reforms and the privatizations so dear to Europe’s institutions. These austerity measures, coming at a time when key economic activity is being sacrificed, will lead to a lengthy recession. The Cypriots all have in mind the example of Greece, where consumption has fallen by more than 30% and GDP by over 25%. This shrinkage will lead to lower tax revenues, a higher debt ratio, etc. Europe will then demand more austerity measures. Seeing another country trapped in this spiral will further discredit the European project.

Some desire to pull out of the euro zone has been simmering since the beginning of the crisis in Cyprus, and there is little chance that it will die out now.

It is therefore necessary to give new opportunities to Cyprus (and to Greece and Portugal and Spain), not the economic and social ruin imposed by the Troika, but an economic revival involving a plan for industrial reconversion and reconstruction. For example, the exploitation of the gas fields discovered in 2011 on the south of the island could offer a way out of the crisis. It would still be necessary to finance the investment required to exploit them and generate the financial resources the country needs. It is time to mobilize genuine assistance, a new Marshall Plan financed by the countries running a surplus.

Risk of chain reactions in the banking systems of other Member States: the European authorities must make a major effort at communications to explain this plan, and that is not easy. From this point of view, the first plan was a disaster, as it demonstrated that the guarantee of deposits of less than 100,000 euros can be annulled by tax measures. For the second plan, the authorities must simultaneously explain that the plan is consistent with the principle of the banking union – to make the shareholders, creditors and major depositors pay – while clarifying that it has a specific character – to put an end to a bank, fiscal and regulatory haven, and so will not apply to other countries. Let’s hope that the shareholders, creditors and major depositors in the banks in the other Member States, particularly Spain, will allow themselves to be convinced. Otherwise significant amounts of capital will flee the euro zone.

Risk of weakening the banking union: the Cypriot banking system was of course poorly managed and controlled. It took unnecessary risks by attracting deposits at high rates that it used to make profitable but risky loans, many of which have failed. But the Cypriot banks are also victims of the default on the Greek debt and of the deep-going recession faced by their neighbours. All of Europe is in danger of falling like dominoes: the recession weakens the banks, which can no longer lend, which accentuates the recession, and so on.

Europe plans to establish a banking union that will impose strict standards for banks with respect to crisis resolution measures. Each bank will have to write a “living will” requiring that any losses be borne by its shareholders, creditors and major depositors. The handling of the Cyprus crisis is an illustration of this. Also, the banks that need capital, creditors and deposits to comply with the constraints of Basel III will find it harder to attract them and must pay them high rates that incorporate risk premiums.

The banking union will not be a bed of roses. Bank balance sheets will need to be cleaned up before they get a collective guarantee. This will pose a problem in many countries whose banking sector needs to be reduced and restructured, with all the social and economic problems that entails (Spain, Malta, Slovenia, etc.). There will inevitably be conflicts between the ECB and the countries concerned.

Deposit insurance will long remain the responsibility of the individual country. In any event, it will be necessary in the future banking union to distinguish clearly between deposits guaranteed by public money (which must be reimbursed at limited rates and must not be placed on financial markets) and all the rest. This argues for a rapid implementation of the Liikanen report. But will there be an agreement in Europe on the future structure of the banking sector between countries whose banking systems are so very different?

The Cypriot banks lost heavily in Greece. This argues once again for some re-nationalization of banking activities. Banks run great risks when lending on large foreign markets with which they are not familiar. Allowing banks to attract deposits from non-residents by offering high interest rates or tax or regulatory concessions leads to failures. The banking union must choose between the freedom of establishment (any bank can move freely within the EU countries and conduct whatever activities it chooses) and the principle of liability (countries are responsible for their banking systems, whose size must stay in line with that of the country itself).

In the coming years, the necessary restructuring of the European banking system thus risks undermining the ability of banks to dispense credit at a time when businesses are already reluctant to invest and when countries are being forced to implement drastic austerity plans.

In sum, the principle of making the financial sector pay for its excesses is beginning to take shape in Europe. Unfortunately, the Cyprus crisis shows once again the inconsistencies of European governance: to trigger European solidarity, things had to slide to the very edge, at the risk of going right over the cliff. Furthermore, this solidarity could plunge Cyprus into misery. The lessons of the past three years do not seem to have been fully drawn by Europe’s leaders.

[1] The over 50% reduction of the face value of Greek bonds held by private agents in February 2012 already went in this direction.

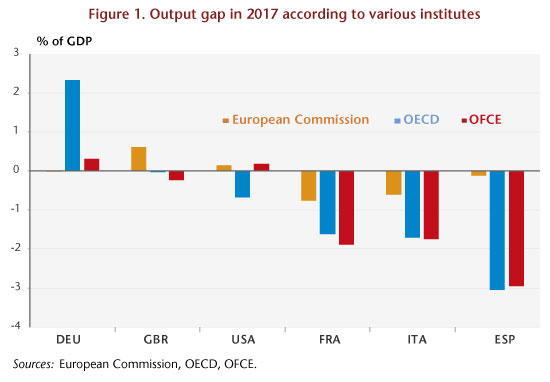

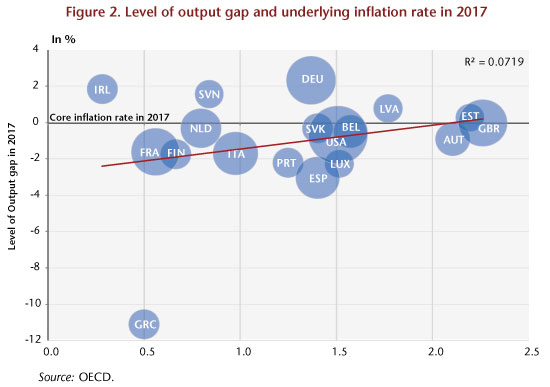

The presence of developed countries in both categories should logically result in the appearance of inflationary pressures in the countries listed in the first group and an inflation gap in those in the latter. However, these two phenomena were not apparent in 2017: as shown in Figure 2, the link between the level of the output gap and the underlying inflation rate is far from clear, casting doubt on the interpretation to be made with respect to the level of the output gap: to uncertainties relating to this notion is added that associated with the level of this gap in the past, in 2007 for example.

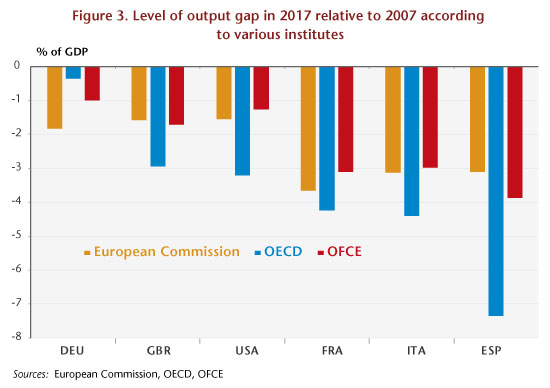

The presence of developed countries in both categories should logically result in the appearance of inflationary pressures in the countries listed in the first group and an inflation gap in those in the latter. However, these two phenomena were not apparent in 2017: as shown in Figure 2, the link between the level of the output gap and the underlying inflation rate is far from clear, casting doubt on the interpretation to be made with respect to the level of the output gap: to uncertainties relating to this notion is added that associated with the level of this gap in the past, in 2007 for example. Given this high level of uncertainty, it seems appropriate to make a diagnosis based on how this output gap has varied since 2007. Such an analysis leads to a clearer consensus between the different institutes and to the disappearance of the first category of countries, those with no additional growth margin beyond their own potential growth. Indeed, according to these, in 2017 none of the major developed countries would have come back to its output gap level of 2007, including Germany. This gap would be around 1 GDP point for Germany, 2 GDP points for the United Kingdom and the United States, more than 3 GDP points for France and Italy and around 5 GDP points for Spain (Figure 3).

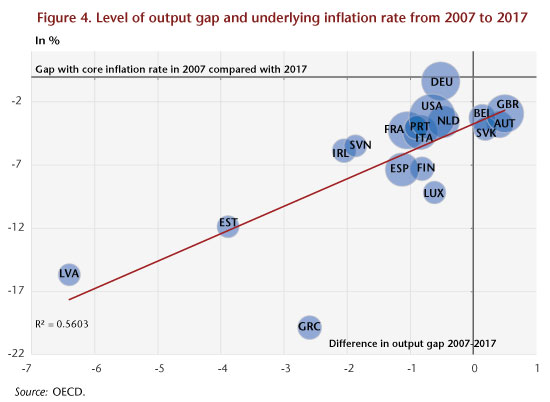

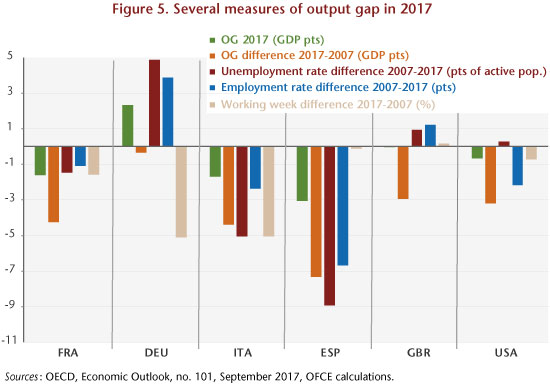

Given this high level of uncertainty, it seems appropriate to make a diagnosis based on how this output gap has varied since 2007. Such an analysis leads to a clearer consensus between the different institutes and to the disappearance of the first category of countries, those with no additional growth margin beyond their own potential growth. Indeed, according to these, in 2017 none of the major developed countries would have come back to its output gap level of 2007, including Germany. This gap would be around 1 GDP point for Germany, 2 GDP points for the United Kingdom and the United States, more than 3 GDP points for France and Italy and around 5 GDP points for Spain (Figure 3). This analysis is more in line with the diagnosis of the renewal of inflation based on the concept of underlying inflation: the fact that the economies of the developed countries had not in 2017 recovered their cyclical level of 2007 explains that inflation rates were lower than those observed during the pre-crisis period (Figure 4). This finding is corroborated by an analysis based on criteria other than the output gap, notably the variation in the unemployment rate and the employment rate since the beginning of the crisis and in the rate of increase in working hours during this same period. Figure 5 illustrates these different criteria. On the basis of these latter criteria, the qualitative diagnosis of the cyclical situation of the different economies points to the existence of relatively high margins for a rebound in Spain, Italy and France. This rebound potential is low in Germany, the United States and the United Kingdom: only an increase in working time in the former or in the employment rate for the latter two could make this possible.

This analysis is more in line with the diagnosis of the renewal of inflation based on the concept of underlying inflation: the fact that the economies of the developed countries had not in 2017 recovered their cyclical level of 2007 explains that inflation rates were lower than those observed during the pre-crisis period (Figure 4). This finding is corroborated by an analysis based on criteria other than the output gap, notably the variation in the unemployment rate and the employment rate since the beginning of the crisis and in the rate of increase in working hours during this same period. Figure 5 illustrates these different criteria. On the basis of these latter criteria, the qualitative diagnosis of the cyclical situation of the different economies points to the existence of relatively high margins for a rebound in Spain, Italy and France. This rebound potential is low in Germany, the United States and the United Kingdom: only an increase in working time in the former or in the employment rate for the latter two could make this possible.