The United Kingdom on the eve of elections: The economy, David Cameron’s trump card (1/2)

In the countdown to the general elections on 7 May 2015, there is so much suspense that the bookmakers are putting the Conservative Party as winners and Ed Miliband, the Labour leader, as the next Prime Minister! Not only are the Labour Party and the Conservative Party running neck-and-neck in the polls, but with voting intentions fluctuating between 30 and 35% for many months now, neither party seems poised to secure a sufficient majority to govern alone. David Cameron, current PM and leader of the Tories, has placed the British economy at the heart of the election campaign. And the figures do seem rather flattering for the outgoing government with regard to growth, employment, unemployment, public deficit reduction, etc., though there are some less visible weaknesses in the UK economy.

A flattering macroeconomic result

With growth of 2.8% in 2014, the UK topped the charts for growth among the G7 countries (just ahead of Canada at 2.5% and the United States at 2.4%). The British economy has been on the road to recovery for two years, as growth picked up from 0.4% yoy in the fourth quarter of 2012 to 3% in the fourth quarter of 2014. This recovery stands in contrast to the situation of the large euro zone economies, where there was a weak recovery in Germany (respectively, 1.5% after 0.4%) and weak growth in France (only 0.4%, against 0.3% in 2012), with Italy still in recession (-0.5% after -2.3%).

At the end of 2014, Britain’s GDP was 5% above its pre-crisis level (i.e. first quarter 2008), due to a strong recovery in services, which was particularly spectacular in business services (where value added (VA) was 20% above its pre-crisis level, representing 12% of VA), with a good performance in the fields of health care (VA 20% above the level of early 2008; 7% of VA) and in real estate (VA 17% above the pre-crisis level; 11% of added value).

According to the initial estimates released on April 28 by the Office of National Statistics (ONS), GDP nevertheless increased by only 0.3% in the first quarter of 2015, instead of 0.6% as in the previous quarters. While this initial estimate is likely to be revised (upwards or downwards, only half of the data on the quarter is known for this first estimate), this slowdown in growth just a few days before the elections comes at a bad time for the outgoing government…

A strong decline in the unemployment rate …

Another highlight of the macro-economic record as the elections approach: the unemployment rate has been falling steadily since late 2011, and was only 5.6% (ILO definition) in February 2015, against 8.4% in late 2011. This rate is one of the lowest in the EU, better than in France (10.6%) and Italy (12.6%), though still behind Germany (only 4.8%). While the unemployment rate has not yet reached its pre-crisis level (5.2%), it is now close. The number of jobs has increased by 1.5 million in the UK since 2011, and David Cameron unhesitatingly boasts of the UK’s success as “the jobs factory of Europe”, creating more jobs on its own than the rest of Europe combined! [1]

Behind this strong increase in employment, however, there are many grey areas…. First, the nature of the jobs created: 1/3 of the jobs created during this recovery are individual entrepreneurs, who now represent 15% of total employment. In times of crisis, a rise in the number of the self-employed generally reflects hidden unemployment, although according to a recent study by the Bank of England[2] this increase is part of a trend. The issue of the growth in what are called “zero hour” contracts, which are contracts for jobs with no guaranteed number of hours, has also burst into the discussion. Until 2013, this type of contract was not subject to statistical monitoring, but according to surveys recently released by the ONS, 697,000 households were affected by this type of contract (representing 2.3% of employment) in the fourth quarter of 2014, against 586,000 (1.9% of employment) a year earlier, i.e. an increase of 111,000 persons, while total employment increased by 600,000 over the period: zero-hours contracts therefore concern only a relatively small portion of the jobs created.

One corollary of the job creation that has taken place since 2011 is low gains in productivity. The British economy began to create jobs from the beginning of the recovery, while productivity fell sharply during the crisis. Companies have kept more employees on the payroll than they usually do in times of crisis, but in return wage increases have been curtailed. UK productivity today remains well below its pre-crisis level. Will the British economy keep a growth model based on low productivity and low wages for a long time to come? It is too early to tell, but this is a subject lying in the background of the election campaign.

Very low inflation

Inflation, as measured by the harmonized index of consumer prices (HICP), fell in February 2015 to only 0% yoy against 1.9% at the end of 2012. This slowdown was due to lower energy prices, but since the end of 2012, also to a slowing in core inflation: from 1.9% at end 2012 to 1.2% in February 2015. The question of inflationary risks has been debated within the UK Monetary Policy Committee for many months now: growth and low unemployment are potentially harbingers of short-term inflationary pressure, if one accepts that the economy is once again approaching full employment. In fact, the continuous decline in inflation since 2012, coming amid low wage increases, a more expensive pound and falling energy prices, has put off the prospect of an acceleration in short-term inflation. For the moment, the members of the Bank of England’s Monetary Policy Committee are voting unanimously for the status quo.

Long-term interest rates on government debt remain at low levels, which was one of the goals hammered at by the Conservatives during the 2010 electoral campaign. In fact, UK rates are moving in much the same way as US rates, in line with similar growth prospects.

Despite this relatively good record, the British economy is still fragile.

The vulnerabilities of the British economy over the medium term

Household debt continues to be high

Household debt had reached record levels before the 2007 crisis, and at that time represented 160% of household annual income. Since then, households have begun to deleverage, with indebtedness falling to 136% at end 2014, which is still well above the 100% level of the 1990s. This deleveraging is lessening households’ vulnerability to a further economic slowdown or to a fall in the price of assets (especially property), but this also has the effect of reining in private domestic demand, while the household savings rate remains low (about 6%) and growth in nominal and real wages moderate. The rebalancing of domestic demand should continue, especially in terms of business investment.

Business investment is catching up

Business investment was structurally weak in the 2000s in the UK. But the recovery has been underway for 5 years, and the rate of investment volume is now close to its level of the early 2000s. The recovery of investment is obviously good news for the UK’s productive capacity. But there is still an external deficit, a sign that the UK is struggling to regain competitiveness, at least with regard to the trade in goods. The stabilization of the trade deficit at around 7 GDP points in 2014, however, was due to the goods deficit being partially offset by a growing surplus in services (5 GDP points at end 2014), a sign that the UK economy still has a high level of specialization in services. Nevertheless, taking into account the balance in income[3], the current account deficit came to 5.5 GDP points, which is high.

The deceptive appearance of the public finances

In 2010, the Tory campaign blamed the previous government for letting the deficits mount during the crisis. Their electoral programme included a large-scale fiscal austerity plan, which corresponded to the archetypical IMF plans: 80% spending cuts and 20% revenue increases over a 5-year horizon. In fact, as soon as they came to power, the government increased the VAT rate, which in 2010-2011 interrupted the recovery; it cut spending, while preserving the public health system (NHS) that the British hold so dear, as well as public pensions, which are low in the UK, but which the government decided to peg to inflation or wages (using whichever is the higher of the two variations, with a guaranteed minimum of 2.5%).

Five years later, David Cameron is highlighting the “success” of his government, which has cut the public deficit in half, from a level of 10% in 2010 to 5.2% in 2014. But with respect to the government’s initial ambitions, this is in fact only a partial success: its first budget in June 2010 set out a public deficit of only 2.2% of GDP in 2014. The originally planned decrease in public expenditure relative to GDP was in fact realized, but revenue rose much less than expected (due in part to sluggish household income).

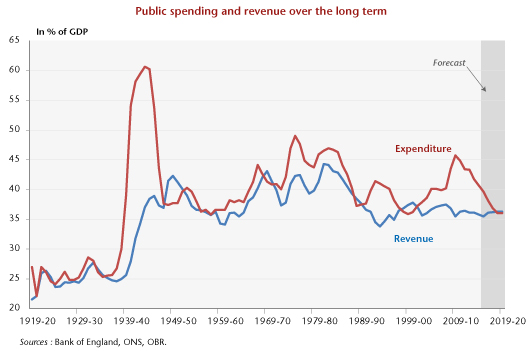

While the austerity programme was generally weaker than what had been announced, in the March 2015 budget the government set out sharp cuts in public spending by 2019, which would bring it down from the current level of 40% of GDP to only 36% of GDP, one of the lowest levels of public spending since World War 2 (graphic). This reduction in public spending would be sufficient in itself to balance the public deficit, without any significant tax hikes: this would represent large-scale budget cuts, whose components are not specified and which it is hard to imagine would not sooner or later affect spending on health care and pensions, which the government has so carefully avoided doing up to now…

[1] “We are the jobs factory of Europe; we’re creating more jobs here than the rest of Europe put together” (Speech on 19 January 2015).

[2] “Self-employment: what can we learn from recent developments?”, Quarterly Bulletin, 2015Q1.

[3] But the deficit of the balance of direct investment income (2 percentage points of GDP) is probably inflated by the relatively good performance of foreign companies operating in the UK in comparison to British companies operating abroad.