What direction for monetary policy in 2022?

With the return of inflation in 2021, the focus is now

on the central banks and their mandate for price stability. Between 15 and 17

December 2021, the Federal Reserve, the Bank of England (BoE), the European

Central Bank (ECB) and the Bank of Japan (BoJ) all held their final monetary

policy meetings of 2021. What do these meetings tell us about their approaches

to asset purchases and monetary policy in 2022? Is a rapid rise in interest

rates on the cards? Despite remaining uncertainty about the future course of

the pandemic and its consequences for activity in the first half of 2022, the central

banks have gradually revised their assessment of the situation with regard to

rising inflation. They now think that the inflationary shock will continue into

2022. Based on this, the British were the first to act as the BoE announced an increase

in its key rate. The Federal Reserve is likely to follow in 2022, presaging future

normalization. As for the ECB, despite winding down its asset purchase

programme linked to the health crisis, it is not yet envisaging the normalization

of monetary policy. In any event, its latest meeting did not suggest a rate

hike in 2022 in the euro zone.

Central banks raise inflation expectations

The recent surge in prices in all the industrialized

and emerging countries is largely due to the rebound in energy and many other commodity

prices in connection with the effects of the health crisis on the global

economic situation in 2020 and 2021.[1] This follows a long period of low inflation,

which led central banks to set their interest rates at a very low level and to

implement unconventional monetary policies such as asset purchase programmes.

These policies, which resulted in sharp increases in their balance sheets, were

aimed at holding down long-term rates.[2] Yet price stability is a key element of the

central banks’ mandate. It is therefore natural that the recent inflationary

pressures raise the question of how they will react and whether they might tighten

their monetary policy stance, since inflation is well above the 2% target

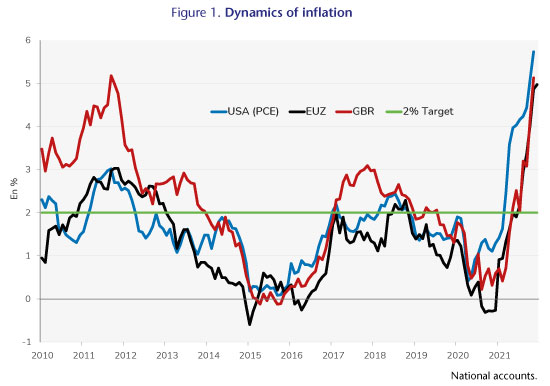

generally used by central banks to judge price stability.[3] Indeed, in December 2021, the year-on-year change

in the consumer price index rose to 5% in the euro zone and, in November, 5.1%

in the UK (Figure 1). In the United States, the consumer price deflator –

an indicator monitored by the Federal Reserve – rose by 5.7%, the highest level

since the early 1980s.[4] Beyond the impact on energy prices, the underlying

indices also rose. In the euro zone, the year-on-year change climbed from 0.4%

in December 2020 to 2.7% a year later, while in the US the underlying

consumption deflator reached 4.7% in November.[5]

While initially the central banks were not all that

concerned about the phenomenon, considering it temporary, it is clear that they

have gradually revised their view, resulting in upward revisions of their

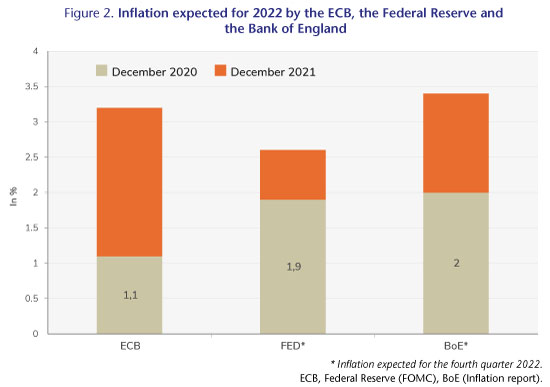

inflation expectations for 2022 (Figure 2). Thus, the inflation projection

that was communicated by the Federal Open Market Committee

(FOMC) in December 2020 for the end of 2022 was 1.9%. One year later, the

inflation forecast for the fourth quarter of 2022 was 2.6%. The ECB has also

issued a significant revision, with inflation expectations rising from 1.1% in

December 2020 to 3.2% – for the year as a whole – according to the latest

projections of December 2021.[6] Inflationary pressure is still considered temporary,

as all three central banks foresee inflation in 2023 closer to the target.[7] Nevertheless,

in the context of a recovery but also of uncertainty about the effects of the

new Omicron variant, the central banks are facing a dilemma. Should they

counter these inflationary pressures by tightening monetary policy? Even if the

rebound in inflation is temporary, inflation would be well above target for

some months, which could lead to second-round effects. Moreover, the

accumulation of household savings could boost growth in 2022 and keep inflation

high.[8]

Conversely, could tightening prematurely undermine the

recovery and slow the fall in the unemployment rate? In this respect, the

unexpected return of inflation could also provide an opportunity to see how the

ECB and the Federal Reserve might adjust their monetary policy after the

announcement of their inflation target revisions. Indeed, in July 2020, the US

central bank announced that it wished to wait for an inflation target of 2% on average, indicating that after being under target,

as was the case in recent years, it would tolerate inflation above 2%. The

rebound in inflation might have suggested that the Federal Reserve would be

less reactive to rising inflation. However, the acceleration of prices has been

significant in the US, and the recent change in tone suggests that even if the

Fed tolerates inflation above 2%, the current level is probably too high.[9] Paradoxically, the ECB has not announced average

inflation targeting (AIT) but has made it clear that the target is 2%

and that it should be interpreted symmetrically. The ECB

therefore considers that inflation below or above 2% is not compatible with its

objective of price stability. Nevertheless, this is a medium-term target and

takes into account lags in the transmission of monetary policy. So even though

the ECB has not indicated that it will tolerate inflation above 2%, it will not

automatically tighten monetary policy when observed inflation exceeds the

target but it will condition its action on its inflation expectations over a 12

to 24-month horizon. Its expectation for 2023 therefore indicates that current

inflation is temporary and that beyond 2022 inflation should again be below 2%.

The Bank of England and Federal Reserve consider

normalization

The communications from the central banks’ monetary

policy meetings held between 15 and 17 December 2021 were expected to focus on

two points: the continuation of their asset purchase programmes and the level

of the key interest rates.

The BoE was the quickest to react by raising its key

rate by 0.15 percentage points, from 0.1% to 0.25%. As stated in its 16 December

press release: “The MPC’s remit is clear that the inflation

target applies at all times, reflecting the primacy of price stability in the

UK monetary policy framework.” Furthermore, it was decided to

maintain the stock of securities acquired by the BoE. A key element of this

decision is the way in which the BoE has implemented its asset purchase policy.

Unlike the Federal Reserve and the ECB, which announce purchase flows on a

monthly basis, the BoE proceeds in stages, announcing a target for the stock of

assets – revised if necessary – and making purchases quickly in order to reach

the target.[10] Moreover, the BoE has not made its rate decisions

conditional on its asset purchase policy, whereas ECB communiqués have always

stated that it would only consider rate hikes once asset purchases have stopped.

In the United States, a rate hike is to be preceded

by a so-called taperingphase during which the Federal Reserve

gradually reduces monthly purchases. The strategy implemented by the US central

bank therefore consists first of all of communicating this path for asset

purchases. This first step was launched in November. At the meeting of 15

December 2021, the FOMC announced that the pace of tapering down was being

accelerated: from January 2022, monthly purchases will be USD 60 billion (40 bn

for Treasuriesand 20 bn for Mortgage-backed Securities)

compared with USD 120 billion per month before November 2021. There will be

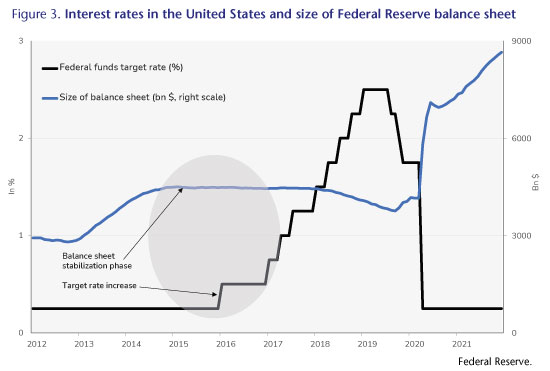

further reductions in the following months. The Federal Reserve is acting in a

sequenced manner, as it did during the previous phase of normalization that

began in January 2014 (Figure 3). Purchases stopped at the end of 2014,

and the policy rate was raised in December 2015. Finally, the reduction in the

size of the balance sheet – in billions of dollars – had been announced in June

2017 and implemented from October 2017.[11] However, the timetable is likely to be

accelerated, as information from the 15 December meeting suggests that there

could be three rate hikes in 2022. The time between the end of asset purchases

and a rate hike would be shortened, and rates would rise more quickly than in

this previous phase of normalization, when there was only one hike in 2015 and

another one a year later. The FOMC members in fact anticipate a target rate for

federal funds of 0.9% at the end of 2022, compared to the current range of

0-0.25%.[12]

It should also be noted that, in accordance with

its mandate, the FOMC is focusing on the situation in the labour market, since

the Federal Reserve must not only ensure price stability but also achieve

maximum employment. In this regard, while the unemployment rate fell to 4.2% in

December, employment remains 1.8% (or 2.8 million jobs) below the December 2019

level, also reflecting withdrawals from the labour force. The prospects of

stabilizing the size of the balance sheet – in value terms – in early 2022 and

of several rate hikes therefore indicate that the Federal Reserve sees labour

market conditions as gradually converging towards the maximum level of

employment.

The ECB takes a more cautious approach

In the euro zone, inflationary pressures have

increased even as the economic recovery remains more fragile. In the third

quarter of 2021, GDP was still 0.3% below its level at the end of 2019, whereas

for the United States it was 1.4% above. There is nevertheless improvement in terms

of the unemployment rate, which in November 2021 stood at 7.3%, lower than the

level observed prior to the outbreak of the pandemic. However, in her press

release at the 16 November press conference, Christine Lagarde considered that

monetary policy must remain accommodating in order to bring inflation down towards

its medium-term target. Thus, beyond the current inflationary pressure, the ECB

still considers that inflation will remain below target in 2023, which

therefore argues for a slower normalization of monetary policy in the euro area.

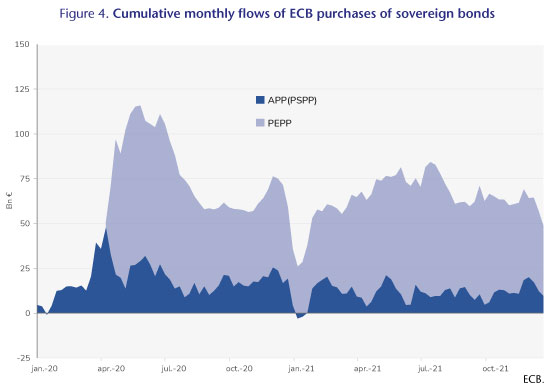

Nevertheless, the Governing Council announced the end of the Pandemic Emergency Purchase Programme (PEPP) in 2022.

The PEPP had been put in place in March 2020, in the context of the pandemic,

to combat sovereign risk.[13] Note that purchases had already slowed in line

with the announcements made since September 2021 (Figure 4). However, this reduction in purchases under

the PEPP would be partly offset by an increase in purchases throughthe Public Sector Purchase Programme

(PSPP). In the second quarter of 2022, purchases are to increase from 20

to 40 billion euros per month. They would then adjust to 20 billion euros in

October 2022, after a plateau of 30 billion euros in the third quarter. At this

stage, the ECB is not indicating a complete halt to asset purchases. The size

of its balance sheet would therefore continue to grow, postponing for the time

being the prospect of a rate hike, probably beyond 2022.[14]

Although there has been talk of normalizing monetary

policy, the central banks remain cautious about the recent inflationary surge,

considering it a temporary episode. The same caution seems to prevail in most

other industrialized countries. In Japan, although inflation is rising (to 0.6%

in December 2021), it remains well below the BoJ’s target. The BoJ has

therefore not changed its communications. Quantitative easing continues, and it

is sticking to the goal of keeping the short-term rate at -0.1% and the

government bond rate at 0%. Earlier this month, the Bank of Canada and the

Australian central bank also maintained their rate targets. The target rose,

however, in Norway.

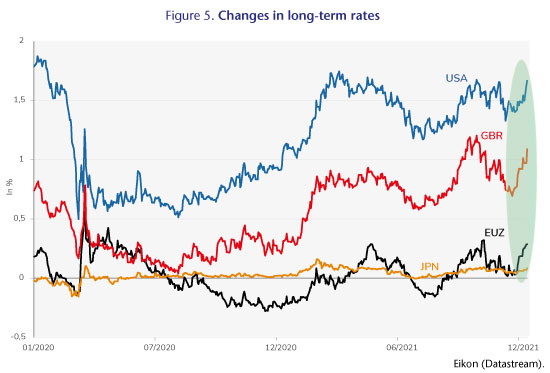

How did the markets react to these policy announcements?

Since 15 December, long-term rates have risen in

the euro zone, the United States and the United Kingdom, approaching the levels

seen before the outbreak of the pandemic (Figure 5). The trend in Japan is

much more modest. The average rate on government bonds issued in the euro zone rose

by 24 basis points, with a slightly larger increase in Italy and Spain than in

Germany and France. In the United States, the increase is comparable: 24 basis

points between 14 December 2021 and 4 January 2022; but the rate is still below

its pre-crisis level. In the UK, it’s risen over 35 basis points. The markets

have therefore incorporated a moderate tightening of monetary policy by 2022.

Should inflation remain at the level observed at the end of 2021, the central

banks could accelerate the pace of monetary policy normalization, either byraising policy rates further or by reducing the

size of their balance sheets, which would probably result in a further rise in

long-term rates.

The year 2022 should therefore be characterized by

a rise in short-term rates and probably also in long-term rates in the UK and

the US. It is clear that the inflationary surge observed since mid-2021 will

lead the central banks, in particular the BoE and the Federal Reserve, to

accelerate the normalization process. Normalization is also important to give

central banks room to manoeuvre in case of new negative shocks. There is,

nevertheless, economic uncertainty due to the arrival of the Omicron variant.

Even if agents have partly adapted to the health restrictions, a slowdown in

growth without a reduction in inflationary pressures would create a more

delicate trade-off for the central banks between their price stability

objective and the need to support the economy.

[1] See the OFCE post

of 17 December 2021 [in French] on this point and the more detailed analysis of

Le Bayon and Péléraux (2021).

[2] The policy rate set by the central banks

represents a target for very short-term market rates. Changes in this rate are

then intended to influence bank rates and all market rates along the term

structure.

[3] The Federal Reserve and the ECB have recently reaffirmed

the symmetry of this objective by revising their inflation targets.

[4] Inflation measured by the consumer price index rose

by 7.1% in December.

[5] In December 2021, the consumer price index

adjusted for food and energy prices rose by 5.5%.

[6] The way that inflation expectations are determined

differs between the central banks. In the case of the Federal Reserve,

expectations are formulated by the members of the FOMC, while for the ECB they

are formulated by its own economists.

[7] Respectively, 2.3% and 2.2% at the end of the year

in the US and UK, and 1.8% for the year as a whole in the euro zone.

[8] See our October 2021 economic forecasts published

in Policy Brief no. 94: Le prix de la reprise [The Price of the Recovery].

[9] See the OFCE post

of 4 January 2022 on inflation targets and expectations [in French] and the

detailed analysis of Blot, Bozou and Hubert (2021).

[10] See Gagnon and Sack (2018) for a comparison of these two strategies.

[11] Measured in GDP points, the size of the balance

sheet fell slightly earlier, from 26.4% in Q1 2015 to 18.8% in Q2 2019. Prior

to the implementation of unconventional measures, the Federal Reserve’s balance

sheet was between 6% and 7% of GDP.

[12] This is the scenario that emerges from the Minutes. The Federal Reserve publishes a detailed report

of the FOMC meeting three weeks following the meeting.

[13] See Blot, Bozou, Creel and Hubert (2021) for a more in-depth discussion of the

objectives and effects of the ECB’s sovereign asset purchase programmes.

[14] The 16 December press release does indeed state

that: “We expect net purchases to end shortly before we start raising the

key ECB interest rates.”