by Christophe Blot, Caroline Bozou and Jérôme Creel

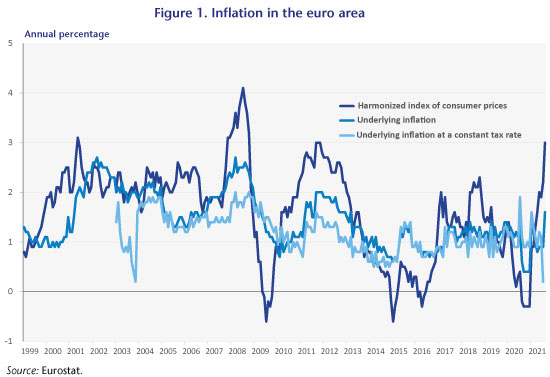

In August 2021, inflation in the euro area reached 3% year-on-year. This level, which has not been seen since November 2011, exceeds the European Central Bank’s target of 2%. This recent momentum is being driven partly by oil prices, but there has been a simultaneous rebound in underlying inflation, which excludes the energy and food price indices from the calculation. Inflation in the United States is also returning to levels not seen for several years, fuelling the debate on a potential return of inflationary risks. Given the central banks’ mandate to maintain price stability, it is legitimate for them to examine the sources of renewed inflation. In a recent paper in preparation for the Monetary Dialogue between the European Parliament and the ECB, we discuss the temporary rather than permanent nature of this episode of inflation.

The recent development of inflation cannot be dissociated from the overall economic situation, which today is still strongly affected by the health crisis. After a sharp fall in activity – GDP contracted by 6.5% in 2020 – the macroeconomic performance of the euro area remains erratic. The crisis has been unprecedented both in terms of its scale and in terms of its sectoral characteristics and the nature of the shocks that have hit the euro area economies. The Covid-19 crisis has in reality been characterised by a simultaneous negative shock to both supply and demand (see Dauvin and Sampognaro, 2021).

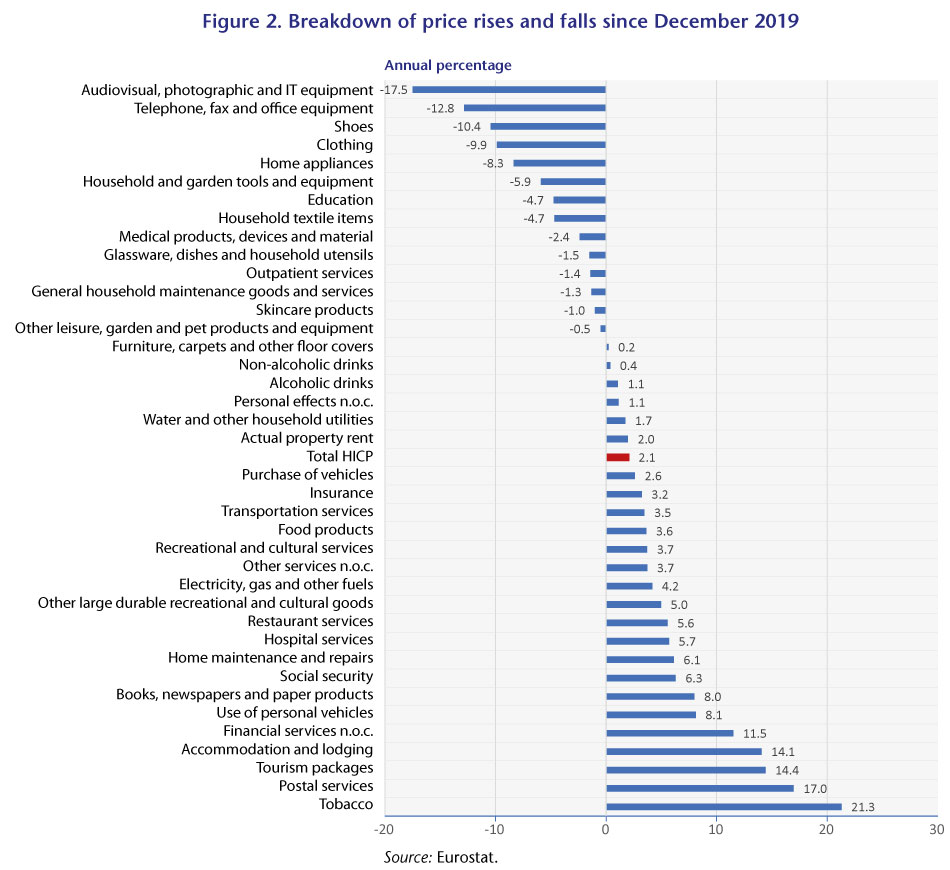

The factors driving current inflation appear to be temporary in nature. Indeed, a review of recent data suggests that the rise in inflation is mainly due to energy prices, to changes in Value-Added Tax rates and to the recovery from the most dramatic one-year recession since World War II (Figure 1). However, at a disaggregated level, it appears that for most goods, prices are often below the December 2019 level, while prices for some services are higher (Figure 2).

Nevertheless, there are many factors that could influence inflation over the medium term, and they leave some uncertainty about future pressure. The demand shock from the European fiscal stimulus and from labour market pressures is likely to be small. The inflationary cost of a fall in euro area unemployment is now very low – there is talk of a flattening of the Phillips curve, see Bobeica, Hartwig, and Nickel, 2021) – and job vacancies, though high, are below the levels of 2018 when there were no fears of a return of inflation. However, agents’ dissaving behaviour is generating inflationary pressures that could herald a more uncertain path. A surge in demand could fuel future price increases, especially if the difficulties in supply adjustment observed recently in certain sectors were to persist. As for supply difficulties and the rising cost of maritime transport, the latter’s strong correlation with oil prices suggests this will fall over the next two years (see the US Energy Information Administration bulletin).

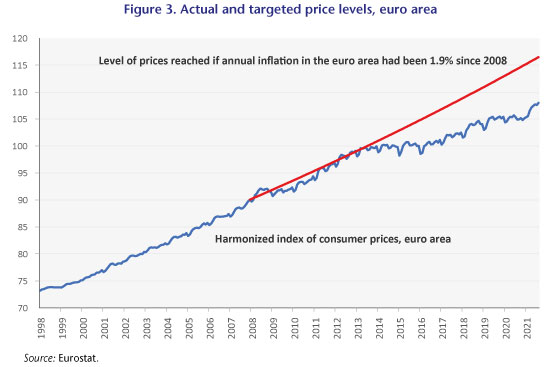

However, if we take a longer view, we can see that the upturn in inflation in no way makes up for the many years during which inflation fell below the 2% target (Figure 3). Thus, as long as the surge observed in recent months remains contained, this return of inflation could be seen as good news for the ECB, enabling it to finally reach its target and even possibly make up for past under-adjustments.