Austerity in Europe: a change of course?

By Marion Cochard and Danielle Schweisguth On 29 May, the European Commission sent the members of the European Union its new economic policy recommendations. In these […]

By Marion Cochard and Danielle Schweisguth On 29 May, the European Commission sent the members of the European Union its new economic policy recommendations. In these […]

By Marion Cochard and Danielle Schweisguth On 29 May, the European Commission sent the members of the European Union its new economic policy recommendations. As part […]

By Guillaume Allègre In a forthcoming article in the Journal of Economic Perspectives[1], Harvard Professor and bestselling textbook author Greg Mankiw defends the income earned […]

By Evens Saliesa The challenge facing policy-making on the reduction of greenhouse gas emissions is not just environmental. It is also necessary to stimulate innovation, a […]

By Pierre Madec As the Governor of the Bank of France and the Minister of the Economy and Finance announced a further (probable) reduction in […]

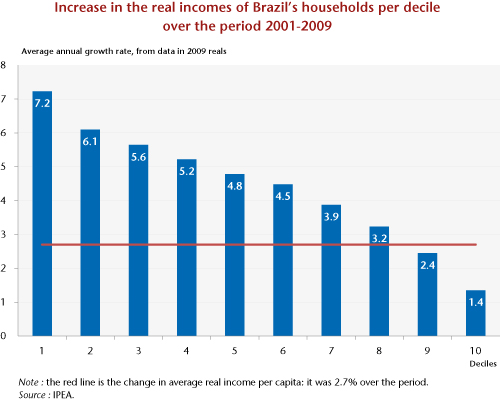

By Christine Rifflart The rise in public transport prices had barely been in force for two weeks when this lit the fire of revolt and […]

by Philippe Weil The bill to promote access to housing and urban renovation provides for regulating rents “mainly in urban areas where there is a […]

By Jean-Luc Gaffard The concept of a “vertical network” [filière] is back in the spotlight and is playing the role of an instrument of the […]

By Céline Antonin and Sandrine Levasseur On 1 July 2013, ten years after filing its application to join the European Union, Croatia will officially become […]

Copyright © 2025 | WordPress Theme by MH Themes