Has the 35-hour work week really “weighed down” the French economy?

By Eric Heyer Did the Aubry laws introducing the 35-hour work week in France between 1998 and 2002 really make French business less competitive and […]

By Eric Heyer Did the Aubry laws introducing the 35-hour work week in France between 1998 and 2002 really make French business less competitive and […]

By Marion Cochard and Danielle Schweisguth On 29 May, the European Commission sent the members of the European Union its new economic policy recommendations. In these […]

By Marion Cochard and Danielle Schweisguth On 29 May, the European Commission sent the members of the European Union its new economic policy recommendations. As part […]

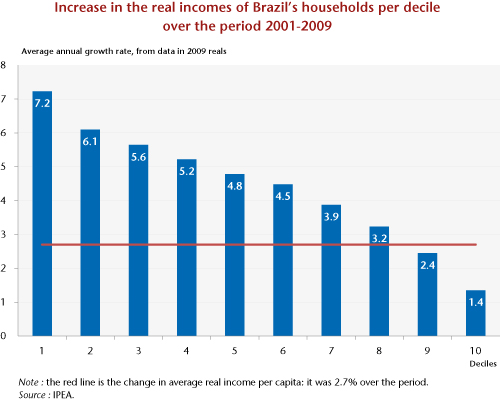

By Christine Rifflart The rise in public transport prices had barely been in force for two weeks when this lit the fire of revolt and […]

By Céline Antonin, Christophe Blot, Sabine Le Bayon and Catherine Mathieu The crisis affecting the euro zone is the result of macroeconomic and financial imbalances […]

By Eric Heyer “France should copy Germany’s reforms to thrive”, Gerhard Schröder entitled an opinion piece in the Financial Times on 5 June 2013. As […]

By Mathieu Plane The figures for French growth for 2014 published by the European Commission (EC) in its last report in May 2013 appear to […]

By Eric Heyer and Hervé Péléraux At the end of 2012, five years after the start of the crisis, France’s GDP has still not returned […]

By Christophe Blot While France has just reaffirmed that it will meet its commitment to reduce its budget deficit to below 3% by 2014 (see […]

By Eric Heyer On April 17, the government presented its Stability Programme for 2013-2017 for the French economy. For the next two years (2013-2014), the government […]

Copyright © 2026 | WordPress Theme by MH Themes