By Christophe Blot, Jérôme Creel, Paul Hubert and Fabien Labondance

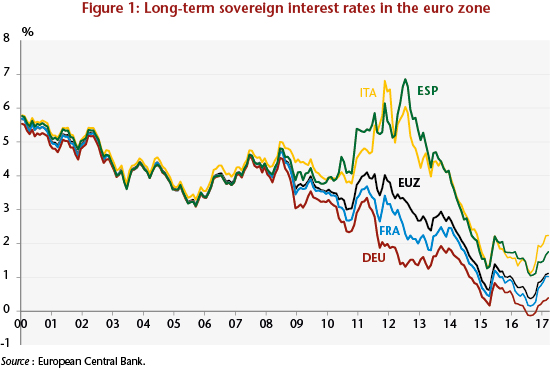

Since the onset of the financial crisis, long-term sovereign interest rates in the euro zone have undergone major fluctuations and periods of great divergence between the member states, in particular between 2010 and 2013 (Figure 1). Long-term rates began to fall sharply after July 2012 and Mario Draghi’s famous “whatever it takes”. Despite the implementation and expansion of the Public Sector Purchase Programme (PSPP) in 2015, and although long-term sovereign interest rates remain at historically low levels, they have recently risen.

There may be several ways of interpreting this recent rise in long-term sovereign interest rates in the euro zone. Given the current economic and financial situation, it may be that this rise in long-term rates reflects the growth and expectations of rising future growth in the euro zone. Another factor could be that the euro zone bond markets are following the US markets: European rates could be rising as a result of rising US rates despite the divergences between the policy directions of the ECB and of the Fed. The impact of the Fed’s monetary policy on interest rates in the euro zone would thus be stronger than the impact of the ECB’s policy. It might also be possible that the recent rise is not in line with the zone’s fundamentals, which would then jeopardize the recovery from the crisis by making debt reduction more difficult, as public and private debt remains high.

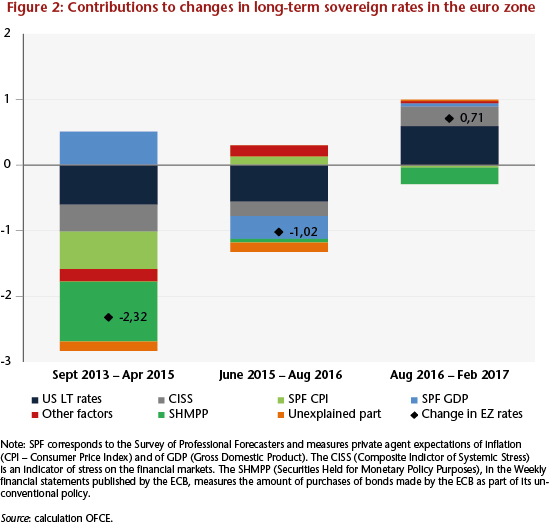

In a recent study, we calculate the contributions of the different determinants of long-term interest rates and highlight the most important ones. Long-term interest rates can respond to private expectations of growth and inflation, to economic fundamentals and to monetary and fiscal policy, both domestic (in the euro zone) and foreign (for example, in the United States). The rates may also react to perceptions of different financial, political and economic risks[1]. Figure 2 shows the main factors that are positively and negatively affecting long-term interest rates in the euro zone over three different periods.

Between September 2013 and April 2015, the euro zone’s long-term interest rate decreased by 2.3 percentage points. During this period, only expectations of GDP growth had a positive impact on interest rates, while all the other factors pushed rates down. In particular, the US long-term interest rate, inflation expectations, the reduction of sovereign risk and the ECB’s unconventional policies all contributed to the decline in euro zone interest rates. Between June 2015 and August 2016, the further decline of about 1 percentage point was due mainly to two factors: the long-term interest rate and the expectations of GDP growth in the United States.

Between August 2016 and February 2017, long-term interest rates rose by 0.7 percentage point. While the ECB’s asset purchase programme helped to reduce the interest rate, two factors combined to push it up. The first is the increase in long-term interest rates in the United States following the Fed’s tightening of monetary policy. The second factor concerned political tensions in France, Italy and Spain, which led to a perception of political risk and higher sovereign risk. While the first factor may continue to push up interest rates in the euro zone, the second should drive them down given the results of the French presidential elections.

[1] The estimate of the equation for the determination of long-term rates was calculated over the period January 1999 – February 2017 and accounts for 96% of the change in long-term rates over the period. For details on the variables used and the parameters estimated, see the study.

Leave a Reply