By Christophe Blot and Paul Hubert

In response to the health and economic crisis, governments have implemented numerous emergency measures that have pushed public debt up steeply. They have nevertheless not experienced any real difficulty in financing these massive new issues: despite record levels of public debt, the cost has fallen sharply (see Plus ou moins de dette publique en France ?, by Xavier Ragot). This trend is the result of structural factors related to an abundance of savings globally and to strong demand for secure liquid assets, characteristics that are generally met by government securities. The trend is also related to the securities purchasing programmes of the central banks, which have been stepped up since the outbreak of the pandemic. For the year 2020 as a whole, the European Central Bank acquired nearly 800 billion euros worth of securities issued by the governments of the euro zone countries. In these circumstances, the central banks are holding an increasingly high fraction of the debt stock, leading to a de facto coordination of monetary and fiscal policies.

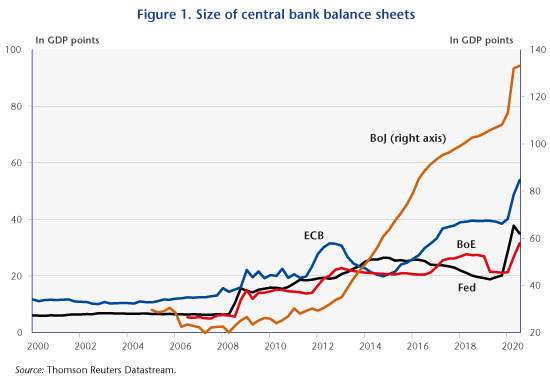

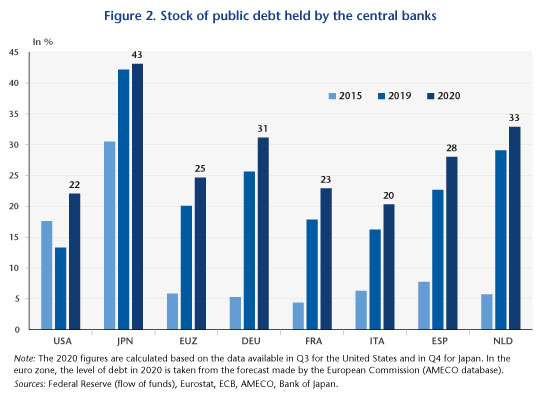

Back in 2009, central banks launched asset purchase programmes to reinforce the expansionary impact of monetary policy in a context where the banks’ key interest rates had reached a level close to 0%[1]. The stated objective was mainly to ease financing conditions by holding down long-term interest rates on the markets. This resulted in a sharp increase in the size of the banks’ balance sheets, which now represents more than 53 GDP points in the euro zone and 35 points in the United States, with the record being held by the Bank of Japan, at 133 GDP points (Figure 1). These programmes, financed by issuing reserves, have focused heavily on government securities, meaning that a large proportion of the stock of government debt is now held by central banks (Figure 2). This proportion reaches 43% in Japan, 22% in the United States and 25% in the euro zone. In the euro zone, in the absence of euro bonds, the distribution of securities purchases depends on the share of each national central bank in the ECB’s capital. The ECB’s distribution key stipulates that the purchases are to be made pro rata to the share of the ECB’s capital held by the national central banks[2]. Consequently, the purchases of securities are independent of the levels and trajectories of public debt. As the latter are heterogeneous, there are differences in the share of public debt held by the national central banks [3]. Thus, 31% of Germany’s public debt is held by the Eurosystem compared to 20% of Italy’s public debt.

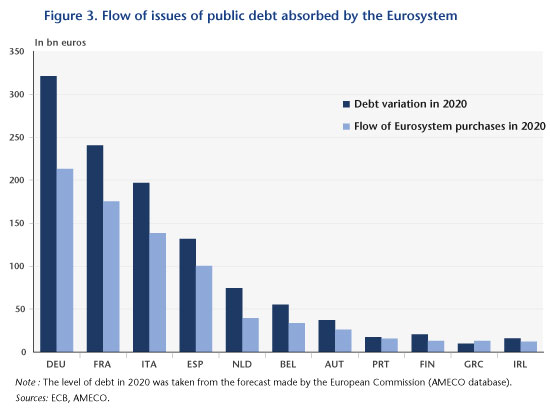

The decentralization of fiscal policies in the euro zone is also leading to tensions in the sovereign debt markets of some member countries, as seen between 2010 and 2012 and more recently in March 2020. This is why Christine Lagarde has launched a new asset purchase programme called the Pandemic emergency purchase programme (PEPP). While the distribution key is not formally abolished, it may be applied more flexibly in order to allow the ECB to reduce the sovereign spreads between member countries. Analysing the flows of securities purchases made by the euro zone central banks and the debt issues of the member states, it can be seen that the Eurosystem has absorbed on average 72% of the public debt issued in 2020, i.e. 830 billion euros out of the 1155 billion of additional public debt. The share amounts to 76% for Spain, 73% for France, 70% for Italy and 66% for Germany (Figure 3).

Unlike purchases made under the APP programme, which aim to hit the inflation target, the PEPP’s objective is first and foremost to limit rate spreads, as Christine Lagarde reminded us on 16 July 2020. In fact, even if there is a structural downward trend in interest rates, some markets may be exposed to pressure. The euro zone countries are all the more exposed as investors can arbitrate between the different markets without incurring any exchange rate risks. This is why they may prefer German securities to Italian securities, thereby undermining the homogeneous transmission of monetary policy within the euro zone. In addition to arguments about the risk of fragmentation, these operations also reflect a form of implicit coordination between the single monetary policy and fiscal policies, providing countries with the manoeuvring room needed to take the measures required to deal with the health and economic crisis. By declaring on 10 December that the allocation to the programme would increase to 1850 billion euros by no later than March 2022, the ECB sent a signal that it would maintain its support throughout the duration of the pandemic[4].

[1] This policy, generally referred to as quantitative easing (QE), was launched in March 2009 by the Bank of England and the US Federal Reserve. Japan had already initiated this type of so-called unconventional measure between 2001 and 2006, and resumed this approach in October 2010. As for the ECB, the first purchases of securities targeted at certain countries in crisis were made from May 2010. But it was not until March 2015 that a QE programme comparable to those implemented by the other major central banks was developed.

[2] In practice, this share is relatively close to the weight of each member country’s GDP in euro zone GDP.

[3] Securities purchasing operations are decentralized at the level of the national central banks. Doing this reduces risk-sharing within the Eurosystem since any losses would be borne by the national central banks, unlike assets held directly by the ECB, for which there is risk-sharing that depends on the share of each national central bank in the ECB’s capital.

[4] The initial allocation was 750 billion euros, which was increased in June 2020 by a further 600 billion. As of 31 December 2020, securities purchases under the PEPP came to 650 billion.

Leave a Reply